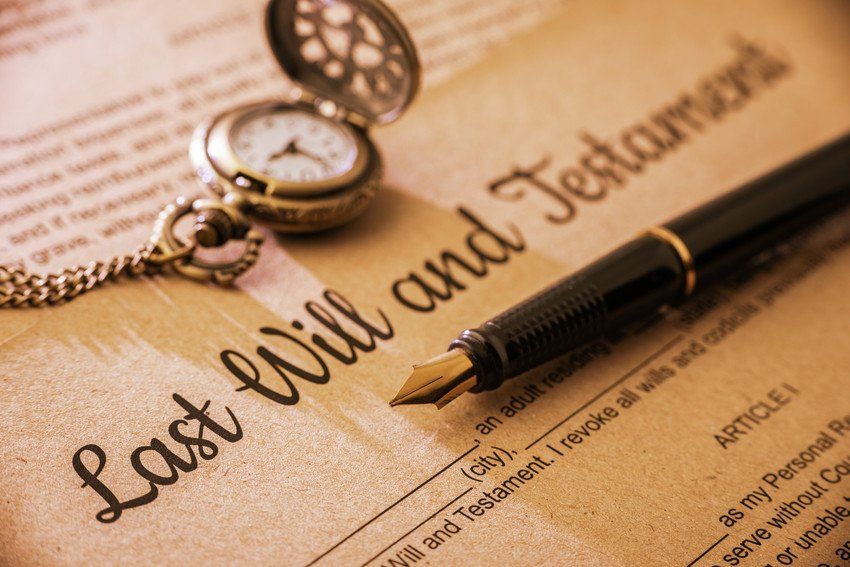

Almy & Thomas notice that some of our colleagues in other practices do not publish details of their costs specifically relating to the preparation and drafting of Wills and the preparation and application for Lasting Powers of Attorney, which are significant steps in anybody’s day to day life. Almy & Thomas are transparent as to the costs of preparing Wills and Lasting Powers of Attorney. Visit our Costs Page and make an appointment to discuss your requirements with Flis Cotton (Head of Department), Kirsty Neill (Assistant Head) or Sophie Lansdale. They will explain and quote for any work that needs to be undertaken in that respect

Buying your first home? Discover the essentials of conveyancing, from fees to finding the right solicitor, with this expert guide from Almy & Thomas.

The office will be closed for the Christmas break from 12:00 Noon on Friday 20th December 2024 and will re-open at 9:00am on Thursday 2nd January 2025. We would like to wish all our current, past and future clients a very Merry Christmas and a Happy New Year.

If you’re about to sign a legally binding contract, then it is important to ensure that all your questions have been answered - read on to find out more.

Are you looking for assistance navigating the buoyant property market? Our expert conveyancing solicitors can help. Get in touch with us today.

A news items appears in the Daily Telegraph whereby a widower who has been given a life interest in the family home by his Deceased Wife is challenging the limited benefits of that bequest on the basis that he was married to his Wife for a number of years. To the shock and horror of his family he has made a claim for family provision to seek a capital sum from his Wife’s Estate. This is a timely reminder that your last will and testament is definitely not necessarily the case. You need to make provision in your will for those that should be reasonably within your consideration at the time of your death. To effectively deny your surviving spouse gives rise to a claim for at least 50% of the Deceased’s Estate. We are not sure why the family are horrified that their father would make such a claim.

We read with some amusement the recommendation of Martin Lewis to say that a very simple way of mitigating Inheritance Tax is to get married! We are not sure that that dramatic step is the better way of mitigating Inheritance Tax. Our Divorce Department would suggest that it can create as much problems as it solves. The adviser goes on to say that once you have married you can give as much money away as you want without giving rise to a liability for Inheritance Tax. That again is wrong. If you do require advice as to mitigating Inheritance Tax, please contact Mrs. Cotton in our Private Client Department on 01803 299131.

Learn essential steps to take if involved in a personal injury claim. Discover how Almy & Thomas, personal injury solicitors in Torquay, can assist you.

Explore mediation and court action for resolving family disputes. Understand their differences and how Almy & Thomas can assist you in family law matters.

There are lots of different types of personal injury claims, where these can be related to your work or to medical malpractice - read on to find out more.